On Mar. 31, Moody’s assigned provisional Ba2 ratings to up to $100 million in taxable revenue bonds for the Waverose Finance Project. The bonds are secured by a loan to NH CleanSpark Borrower Trust 2026-1, with Bitcoin (BTC) as the pledged collateral.

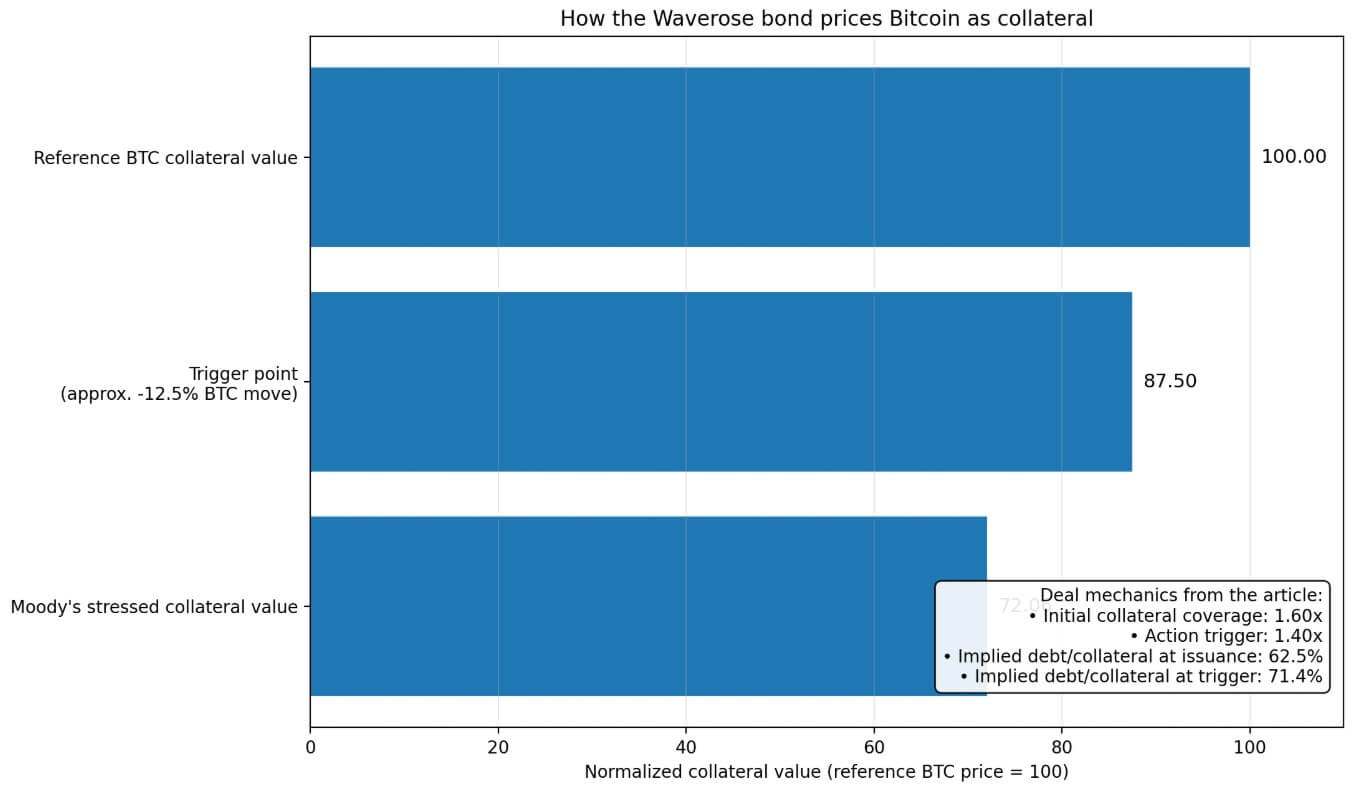

Those numbers set the conditions under which traditional finance agreed to work with Bitcoin at all: 72.06 cents of credit for every dollar of collateral value, a two-day exposure window to act on price moves, and 1.60x initial collateral coverage, which forces action when it drops to 1.40x.

Bitcoin has spent years auditioning for legitimacy as a store of value, a corporate treasury reserve, and an ETF asset. The New Hampshire deal points to Bitcoin as collateral.

Collateral is where an asset earns credit utility, something institutions can borrow against inside structures that credit markets can understand, price, and, when necessary, liquidate fast. That is the line Bitcoin just crossed.

Why this matters: This is the first time Bitcoin has been formally translated into credit terms that public markets understand. Instead of being held or traded, BTC is now being assigned a borrowing value, a liquidation threshold, and a stress price, turning it from an asset into usable financial collateral. That shift opens a new source of liquidity for holders, but also introduces a system where price drops can trigger automatic selling across multiple structures at once.

The opening price of trust

The Waverose structure is a taxable conduit revenue bond.

New Hampshire’s role ends at the conduit, and bondholders carry all loss risk. This is limited-recourse, institutional plumbing.

Two things follow from that structure. First, it keeps risk quarantined: if the collateral breaks down, bondholders absorb the loss. Second, it lays out the precise terms on which traditional finance decided Bitcoin could enter the credit system.

At 1.60x initial collateral coverage, the bond starts with debt equal to about 62.5% of collateral value. The 1.40x trigger, at which automatic action kicks in, implies a debt of roughly 71.4%.

The structure hits its wire trip when BTC falls by approximately 12.5% from issuance pricing, a move Bitcoin has executed routinely.

Moody’s stressed the collateral value at 72.06% of the market price. Mapped to Bitcoin’s Apr. 1 price in the $68,000 zone, the stress zone lands near $49,600.

Standard Chartered put its near-term bear case for Bitcoin at $50,000, and the traditional finance firms calibrated their first public finance haircut on Bitcoin almost exactly on top of a downside path that one of the world’s largest banks still considers reachable.

From owned to pledged

New Hampshire arrived alongside two other recent moves pointing in the same direction.

In February, S&P assigned the first-ever rating to a structured finance transaction backed by Bitcoin. The transaction was the Ledn Issuer Trust 2026-1, with roughly $199.1 million in loans secured by 4,078.87 BTC, carrying a fair market value of approximately $356.9 million, implying an LTV of about 55.8% at inception.

In March, Better and Coinbase launched what they called the first crypto-backed conforming mortgage, in which a borrower pledges $250,000 in BTC to fund a $100,000 down payment, while the first lien stays Fannie Mae-backed.

Bitcoin received three credit wrappers in roughly six weeks, each with different haircuts, liquidation mechanics, and regulatory constraints. Together, they describe a process in which Bitcoin enters credit markets through multiple doors at once, and those doors are edging closer to ordinary household finance.

| Structure | Date | Wrapper type | Collateral / pledge | Haircut / Lationale | Who bears risk | Why it matters |

|---|---|---|---|---|---|---|

| Waverose / New Hampshire | Mar. 31, 2026 | Taxable conduit revenue bond | Bitcoin pledged as collateral for bonds secured by a loan to NH CleanSpark Borrower Trust 2026-1 | Moody’s stressed collateral at 72.06% of market value; 1.60x initial collateral coverage; action triggered at 1.40x; implied debt-to-collateral starts around 62.5% and rises to 71.4% at trigger | Bondholders absorb losses if collateral fails; no New Hampshire public funds pledged | Shows Bitcoin entering public-finance-adjacent credit as rated collateral, not just as an owned asset |

| Ledn Issuer Trust 2026-1 | February 2026 | Structured finance / ABS | Roughly $199.1 million in loans secured by 4,078.87 BTC with fair market value of about $356.9 million | About 55.8% LTV at inception | Investors in the structured-finance deal; risk tied to collateral, operations, and liquidation mechanics | Marks Bitcoin’s entry into rated structured finance |

| Better / Coinbase mortgage product | March 2026 | Crypto-backed conforming mortgage / down-payment loan | Borrower pledges $250,000 in BTC to obtain a $100,000 loan for a home down payment, while the first lien remains Fannie Mae-backed | Example implies a 40% advance rate on pledged BTC | Risk sits with the crypto-backed loan structure, while the first mortgage remains separately conforming/Fannie-backed | Pushes Bitcoin collateral closer to household finance and mainstream mortgage plumbing |

The US municipal market carried $4.4 trillion in outstanding bonds as of the fourth quarter of 2025. Households held 48% directly and about 21% through mutual funds.

Munis occupy a specific psychological slot in American savings culture, sitting where advisors park money for clients who want safety adjacent to tax efficiency.

The Waverose bond lands in the taxable conduit corner. Taxable muni issuance ran only about $33 billion in 2025, less than 6% of the market total. At $100 million, this deal represents roughly 0.0023% of the outstanding muni market.

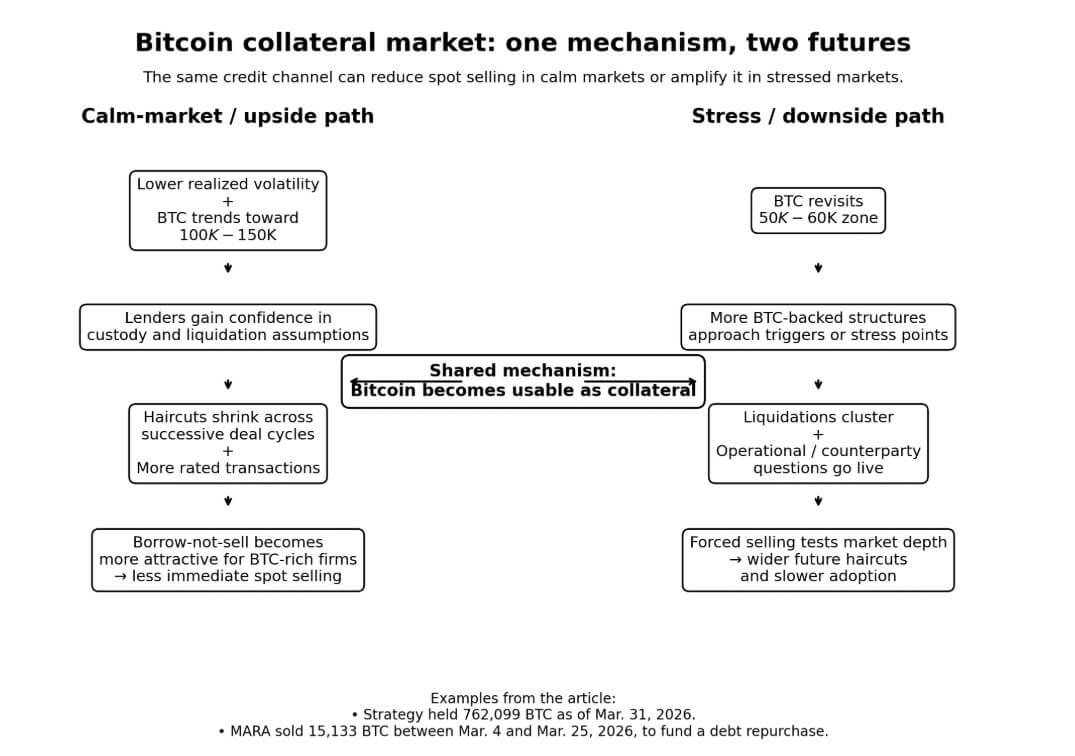

One mechanism for two potential futures

For Bitcoin holders and treasury-heavy firms, collateral utility cuts in opposite directions depending on where the price goes.

Strategy held 762,099 BTC as of Mar. 31. Between Mar. 4 and 25, MARA sold 15,133 BTC for about $1.1 billion to fund a debt repurchase, which were outright spot sales to cover a balance sheet obligation.

A functioning BTC-collateral market sits between the two postures of full accumulation and outright liquidation, while providing credit against reserves that lets holders raise capital while keeping their Bitcoin position.

Fidelity noted in March that public companies and ETFs together hold roughly 12% of Bitcoin’s circulating supply, and that 2025 was Bitcoin’s least volatile year on record, based on annualized realized volatility.

If that holds and Bitcoin trades toward the $100,000-$150,000 range Bernstein projected for late 2026, the collateral channel becomes genuinely attractive. BTC-rich firms carry large reserves at lower realized volatility, lenders build confidence in liquidation assumptions, and the haircut required to access credit shrinks across successive deal cycles.

Each rated transaction adds data to Bitcoin’s nearly empty track record as pledged collateral. A second deal, a third, a cluster, and the pricing of trust starts to compress.

The bear case runs through the opposite direction of the same mechanism. Bitcoin revisiting $50,000, near Standard Chartered’s downside projection and close to the Moody’s stress zone from current prices, turns the operational question live.

Firms start to wonder whether the liquidation mechanics work cleanly when every BTC-backed structure needs to exit at once.

S&P’s rating work on the Ledn ABS flagged operational and counterparty risk, event risk, and liquidation mechanics as the core uncertainties for Bitcoin-backed credit. It noted the market’s ability to absorb forced selling from multiple structures tripping triggers inside the same price window.

A structure that reduces forced selling in calm markets can concentrate it in turbulent ones. That is the inherent geometry of collateralized credit, and Bitcoin’s volatility makes the geometry sharper than it would be for any conventional pledged asset.

The first version of Bitcoin-backed public finance is small, speculative-grade, and built for taxable conduit territory. The architecture is constrained because those constraints were the only terms on which the credit system would engage.

What Moody’s released on Mar. 31 was a pricing schedule for Bitcoin’s entry into credit markets: the conditions under which bond investors set for accepting it as collateral.

Future deals will be negotiated on that schedule, tightening haircuts if volatility falls, widening them if it rises, testing different custody arrangements, and pushing toward the investment-grade boundary.

Each iteration adds institutional memory to a market that currently has almost none.

Bitcoin took years to become something institutions could buy through regulated channels. Becoming something they can lend against will follow the same logic of incremental, conditional growth, built on an accumulating track record.